The Eurozone has been troubled by stagnating growth and low inflation since 2013 and we still haven’t fixed problems of high national debt. In order to evade another economic earthquake similar to or even bigger than the Greek crisis and to reinstate the trust in the Euro, the European Central Bank (ECB) took extraordinary measures to boost growth, raise inflation and indirectly lower the indebtedness of the Eurozone Member States: they started the Quantitative Easing (QE) programme.

What is Quantitative Easing (QE)?

Quantitative Easing is a monetary policy used in extreme circumstances, when regular policies of the central banks are ineffective. Since the Eurozone has been in an economic stagnation for longer than five years, the ECB decided to bring out the big guns.

In short, the ECB is printing money and sending it to the banks, hoping that they’re going to start offering cheap loans to the citizens and companies, thus kick-starting the economy. The downside? It increases inflation. But that’s actually the goal of ECB’s Quantitative Easing – to raise the annual inflation within the Eurozone from 0.2% to 2%, because having deflation causes the economy to contract, which might lead to even bigger problems.

This way this works is that each country has national debt, also known as government bonds, in the financial markets. Bonds are a financial asset and they can be bought and sold, just like shares of a company. So when a financial organisation (usually a bank or a fund) or private figure buys these bonds, the government will owe them money and must pay interest rates and one day repay back these debts.

Eurozone Quantitative Easing is essentially a bond buying program where the European Central Bank buys back the debt of the 19 governments who use the Euro. So the financial organisations and the people who owned these bonds get their invested money back. In order to do that, the ECB prints money and with it buys back the bonds. This essentially lowers governmental debt and should help the economy work again, because it frees up money which was “stuck”.

By the numbers: the ECB printed 60 billion Euros per month between March 2015 to March 2016, totalling over 700 billion Euros (which is about 5.5% percent of Eurozone’s GDP by 2013 data), hoping to energize the economy. (See also Elin James Jones for a breakdown of QE.)

Yet, the European Central Bank’s QE program failed catastrophically.

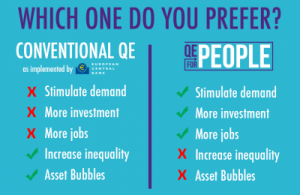

The main task of the ECB is to keep consumer prices stable, which translates to having a secure inflation rate of 2%. Quantitative Easing was meant to raise it to that mark, yet not only did inflation not reach the 2% target, but rather the annual inflation rate went down from 0.2% to 0.1%.

The promised economic growth never showed up – the Eurozone’s economy actually contracted if we’re talking in relative terms: from an average of 1.3% of growth during 9 months before the launch of QE, to only 1% in the months after QE was introduced.

Neither did the ECB’s unorthodox plan help stimulate consumption nor investment in the private sector – both numbers stayed exactly the same in comparison before and after Quantitative Easing[1].

Basic economics tells us that if you print money, inflation is going to rise. But the banks never actually lent any of the printed money, entrepreneurs never tried to take out loans, investors never invested. Those billions of Euros were stashed in Europe’s biggest banks, which started to creat another financial asset bubble, never helped small and medium businesses, and stayed in the pockets of those who could afford to buy government debt. This is the hard reality.

Not only has QE failed completely, but also made the already sore problem of income and wealth inequality greater. Based on the estimations done by the Bank of England, the United Kingdom’s central bank, QE disproportionately benefits the rich. After rolling out QE in 2010, Britain saw its household wealth increase by 600 billion pounds. That would equate to 10,000 pounds per person if the financial gains from QE were evenly distributed across the population. But they were not, since the top 5% of the population owns around 40% of financial assets that are immediately affected by the QuQEprogram.

So has the ECB fixed the QE programme? They’ve improved it, right? No.

Instead of rethinking the core concept of their plan and finding the reasons for its failure, the ECB decided to plow on. On March 2016 they released a statement: monthly QE is going to be increased from 60 to 80 billion Euros and the programme period is going to be prolonged. So instead of stopping trying to fix a broken TV with a hammer, the ECB is going to whack at it with more force until it fixes itself eventually.

Let’s get back to the drawing board

How do we boost growth, lower national and private debt, create jobs, raise investment and lower wealth inequality?

Put yourself into the shoes of the ECB – you have the power to create new money out of thin air which would raise inflation if the money actually reaches the economy. And you have a task: to slowly raise the inflation from 0.1% to 2% and to stimulate growth, job creation and investment. So the problem is quite simple: how to inject the money you created into the economy in the way that would achieve these things most efficiently?

You already know that giving it to the banks and the rich doesn’t work. Out of the question.

You could send the money to the European Union and the Eurozone governments, which they would then reinvest through public projects like building roads, schools and parks. You could even dedicate the money to fight global warming or finance scientific advancement. The money would certainly start to circulate in the economy but lots of it would get wasted due of the nature of central governments and the bureaucracy that comes along.

But there’s even a better and simpler solution – just give it to the people directly. Transfer this printed money directly to the citizens’ bank accounts. Since the ECB is currently printing 80 billion per month, with around 350 million citizens in the Eurozone, everyone would receive 200€ every month. No strings attached – everyone could do whatever they wanted with those 200€ per month.

This solution is called Helicopter Money. It was coined by Nobel Prize winner Milton Friedman in 1969 and is being revived by a campaign called Quantitative Easing for People. It was recently described as “an interesting idea” by Mario Draghi, the chief of ECB, even though the heads of ECB have never discussed it formally. And it’s surely not a surprise, since the European Central Bank is notorious for being afraid of trying out anything new.

But why would Helicopter Money work? Because it’s a direct money transfer into the economy. What would be the first thing Eurozone citizens would do with this “free money”? Buy something. Or repay their previous debts. Either way, this money would reach the economy instantly, without anyone in the middle.

Besides raising consumption and kick-starting the economy in the short term, Helicopter Money would benefit the European Union and its citizens in more than a few ways. These packets of 200€ per month would be effective in fighting poverty and would greatly help the weakest members of society, while at the same time easing income inequality across economic classes within each Member State. It would probably be the first time that an EU institution would directly help citizens in the most tangible way possible.

Helicopter Money would make the economic catch-up process of the newest members of the Eurozone faster than it currently is. Imagine what difference it would make to the average Dutch or Luxembourgish citizen compared to the average Latvian or Slovakian citizen.

Not to mention the positive impact of Helicopter Money on southern Eurozone members that have been hit the hardest during the sovereign debt crisis. It would ease the debt ratio of citizens and help their governments save money without cutting already thin social spending.

At what cost?

Well, higher inflation – which is precisely what we lack of right now.There’s just one question left: how do we control such inflation for it not to exceed 2%? This question is especially important to the German citizens and their government, since they still remember the devastating effect of hyperinflation.

The ECB would always have the capacity to slow down or even cancel Helicopter Money, because of the nature of monthly payments. If, for example, the inflation would exceed the 2% we need, we could immediately stop the program, but based on the experiences of the United States, Britain, Japan and the European Union with Quantitative Easing, there is very little chance of that happening.

But the most exciting outcome of Helicopter Money would be the political impact it would make. It would be the first step towards a Fiscal Union that the Eurozone so desperately needs, just without the unpopular drawback of taxing anyone or redistributing wealth across the continent. Helicopter Money may very well be the next step towards a more equal and integrated European Union.

Helicopter Money is supported by over 75 economists all over Europe. They see Quantitative Easing as a necessity.

With one economic policy we could help solve a great many issues currently facing the Eurozone – slow growth, low inflation, high private and national debts, easing of the Greek crisis, lower income and wealth inequalities, and reduced overall poverty. We must make rational and logical decisions, and enact policy that works for everyone and not just for the rich.

What do we, the citizens of the Eurozone countries, need to do to get Helicopter Money? Even though the European Central Bank is not a directly democratic institution, it has a responsibility to represent the citizens of the Euro area. Big enough popular support for campaigns like Quantitative Easing for People can send a strong message to the institution. Helicopter Money is already being championed by economists and Members of the European Parliament, so all that is left is to amp up the volume[2] and to keep the debate alive. It is time to start implementing policies that work.

This article was originally published on Why Go Federal Europe.

Notes

[1] For more signs of QE failing and a deeper analysis, see here (http://www.qe4people.eu/one-year-of-qe-seven-ways-it-fails)

[2] Stay informed at www.qe4people.eu and on the campaign’s Facebook page.