Reports on the world’s unfolding food crisis have revolved around the war in Ukraine and the blockade of Ukrainian grain exports. But the conflict is only the latest tipping point for a global food system already on the edge. Jennifer Kwao explains why the roots of the food crisis lie in the structures of the world economy. Only by addressing food insecurity as a systemic issue can the EU credibly respond.

On August 1, a ship carrying 26,527 tonnes of corn left Odesa for Lebanon. That’s five months since Putin’s invasion of Ukraine laid siege to all exports of vital foodstuff leaving Ukrainian ports. Putin’s war directly put a stop to the export of grains, sunflower, and fertiliser that millions in the Global South depended on each month. In the past months, the UN and Turkey have been working to create safe corridors for the passage of agricultural exports amid a worsening food crisis, culminating in a deal in Istanbul. However, before the ink on this deal could dry, Russia rained missiles on the port of Odesa.

After sabotaging this deal that had released some 20 million tons of grain stuck at Ukrainian ports, Russia then embarked on a PR tour of Africa that spun the story, and some African leaders bought the narrative. Not only is the Global South facing a humanitarian crisis, but their food security is being thrown into a cynical geopolitical game.

The dramatic situation and lack of concerted response have led the UN and Red Cross to sound the alarm about a silent humanitarian disaster. The message from the UN and the Red Cross has been clear and consistent since the start of the war: this is just one shock to the food security of the Global South. With an estimated 11 people dying every minute from hunger and malnutrition a constant prospect for millions, it is high time to look more seriously at the food crisis; not as an unfortunate outcome of the war in Ukraine or another ailment of distant lands, but as the result of a deeply flawed food system that the Global North has been complicit in cultivating. For countries in Europe, this lens is the only way to present credible solutions and stand out as reliable partners in a time of crisis.

The impacts of the war in Ukraine

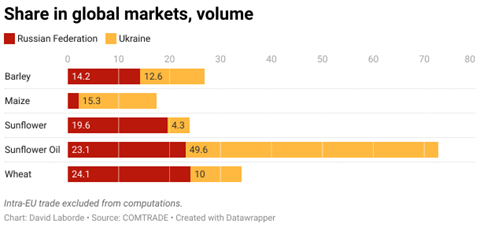

As the top global exporters of wheat, barley, sunflower and maize and fertiliser, Russia’s invasion of Ukraine has tipped the world into a food crisis.

Russia’s strategy has seen the shelling of industries key to the Ukrainian economy and the planting of mines in the Black Sea, Ukraine’s main export route. Besides destroying infrastructure like ports and roads, which are critical to a functioning export industry, this campaign has led to suspended oilseed processing and issuing of export licenses. Since February, trade through the Black Sea has grounded to a halt, causing a sharp decline in the export of Ukrainian grain and taking tons of products out of circulation in the global agricultural trade. Despite efforts from Ukraine to reroute these goods (through neighbouring countries, or via road and rail), it only manages a third of the 4.5 million monthly grain export it used to trade, leaving 20 million tons of grain stuck in its ports.

The fighting has also presented massive challenges to the agricultural industry in Ukraine. Not only is it shrinking areas where food production and storage can take place, but it is also tightening staff shortages for harvesting and planting. In the coming winter period, Ukraine is already expected to not have the capacity to harvest a significant amount of its winter yields.

The supply gap created by the war, in addition to responses by companies and governments, has contributed to soaring food, agriculture, and energy prices. The UN Food and Agriculture Organization’s risk assessment reports that the supply gap created by the war will likely keep prices well above the average.

The energy fallout of the war has also unsettled food supply chains across the world. While African countries are less dependent on Russian fossil fuels than those in Europe, soaring prices on energy markets determine domestic prices which usually act as a benchmark for food prices too. Price speculation aside, food industries everywhere depend heavily on fossil fuels. Besides playing a key role in the planting, harvesting, and processing of food, petroleum is the key ingredient in fertilisers that industrial farming relies on to produce food. This dependence ensures that spiralling energy cost bites along food supply chains everywhere.

The high cost of fertilisers doesn’t just drive food production costs higher, it also shrinks harvests and yields on a wide range of crops. For Global South farmers, who are the lifeblood of food systems, the disequilibrium between input costs and yield, is a disincentive for planting in the new season. While EU farmers can rely on an additional support package to cope with high input costs, farmers in the Global South can expect no such support from their governments who are in worse shape to provide a safety net due to the current economic downturn.

For countries in the throes of the crisis, therefore, the long term looks grim; not only is the food currently being produced and harvested expensive, but harvest in the next period will likely shrink and remain expensive. Meanwhile, European farmers are expected to produce more grains in 2022 and Russia continues its ban on fertiliser exports despite being the world’s leading exporter of the good.

The high production cost also dissuades partners who might have the capacity to fill the supply gap created by the war. Looking at the harsh weather conditions in much of the world this year and food export restrictions top wheat producers as India have subsequently introduced, it is clear they have ruled out the option of exporting their food stock even if they ramp up domestic production.

Exporting in time of war is a costly business. Not only are Ukrainian producers incurring more costs by re-routing grain or from harvests lying in waste, but those importing their produce incur insurance costs. And in a mined Black Sea, everyone along the food chain is incurring additional and unanticipated costs – often for a lesser quantity of goods. For developing countries, this is a premium they cannot afford.

The war in Ukraine represents a tipping point in a worsening food crisis underpinned by an unequal food system.

These price hikes in the food supply chain have a ripple effect on the markets, putting essentials out of reach of consumers. Presently, food is 42 per cent more expensive than in 2014 to 2016. Food essentials like meat, sugar, cereals, and dairy are at the highest they have been since 1961. Wheat prices globally have jumped to more than 50 per cent and, in comparison to a year ago, wheat is 80 per cent more expensive. A similar trend, although less steep rise, is observed in maize prices on the global market following the war – it is 25 to 30 per cent higher than prices in February.

Besides the price hikes and disruptions to food production and supply, national governments have actively cut supplies. Since March, Russia has banned sugar, rapeseed, and sunflower seeds exports. In the first four months of its unprovoked war, it banned the export of wheat, meslin, rye, barley, maize and sugar. In contrast, Ukraine banned the export of maize, rye, eggs, poultry, sunflower oil, and bovine meat export for two months (from March to May) and has since lifted restrictions.

Amid fears of more shortages, countries such as India, Algeria, and Turkey have self-imposed bans on food exports. Although accounting for a small share of global grain trade, this move means that countries looking elsewhere for large grain imports could not turn to partners in the Global South. In the EU, Hungary has so far been the only country to dapple in these trade restrictions; from March to May, it banned the export of grains and sunflower seeds. Overall, reports of a difficult farming season due to extreme weather in Europe and India deflate hope of these partners stepping in to fill this gap with their surplus.

Who is most impacted

The war in Ukraine has cast a long shadow over food security across the globe but not everyone has been impacted the same way. Not only are countries in the Global South the most impacted, but their most vulnerable populations are at the highest risk of starvation. This unequal impact points to a fundamental problem of inequity in global food markets and food security.

In the Global North, households usually spend 17 per cent of their income on food, whereas their counterparts in the Global South spend a whopping 40 per cent. So while consumers in the Global North may experience the current price hikes as a slight change in their food expenditures – or not feel it at all due to inflated incomes – those in the Global South face an impossible choice between subsistence and other living expenditures. In Nigeria, for example, pasta and bread have become as much as 50 per cent more expensive.

The hardest hit are the countries that were heavily dependent on Ukrainian and Russian food imports. Egypt, Indonesia, Pakistan, Bangladesh, and Lebanon were all top destinations for Ukrainian grains. Notably, the largest wheat importers in the world are on the African continent: Egypt, followed by Algeria and Nigeria. Most countries in Africa are net importers of wheat. In eastern Africa, a third of cereal consumption comes from wheat which is largely imported from Ukraine and Russia – 84 per cent to be exact. In Benin, nearly 100 per cent of wheat imports come from Russia.

And while the market logic of capitalism will have us celebrate this as progress and fair access, the reality is that the availability of food to millions is at the mercy of external shocks whose devastating consequence is playing out before our eyes.

The situation is worst where countries are food import and aid-dependent, and battling climate change, conflicts, and economic recession. The Democratic Republic of Congo, Afghanistan, Somalia, Ethiopia, and Yemen have been named “hunger hotspots” and some of the worst hit by the food crisis.

Alarmingly, the World Food Programme, which feeds 125 million people, buys 50 per cent of its grain from Ukraine. The war, therefore, renders a key crisis mechanism ineffective in meeting the needs of the most vulnerable populations.

How did we get here?

While for some in Europe, the food crisis may seem a sudden, unexpected event, food insecurity was already showing an upward trend as of 2019. In 2020, over 800 million people suffered from hunger. Two-thirds of this food insecure are in Sub-Saharan Africa, India, and China. The Global Report on Food Crises estimates that 193 million people were in an acute food crisis in 2021, with thousands experiencing starvation and death and millions more facing an emergency-level crisis. Why were millions going hungry in a period of relative peace?

Well, it turns out that “a period of relative peace” is a narrow view of the world before the war in Ukraine. For many countries, the period before the war was a sequence of internal conflicts, health crises, extreme weather events, economic downturn, and trade barriers all undermining their food security. The war represents a tipping point in a worsening food crisis underpinned by an unequal food system. The better question is therefore what are the drivers of the unfolding food crisis?

The most recognisable shock to food systems in recent years is the Covid-19 pandemic and the ensuing economic downturn. As the world shut down and millions sought shelter at home, food access become precarious but not for the reasons we previously thought. The latest analysis shows that while pandemic restrictions impacted the availability of food by slowing processing, transport, and trade, the more damaging blow to food security came from the loss of income and rising food prices during the pandemic.

Pandemic restrictions that shut down industries and enforced curfews meant no work for the world’s workers, the majority of whom work in informal sectors. No work meant no income. And no income means no food. Those relying on income from market trading and remittances were especially affected as these activities were reduced or stopped.

While the economic downturn began in epicentres (China, Europe and the US), almost all low to middle-income countries suffered losses in the form of depreciating currencies, rising production costs, high unemployment, and lower demands for their exports.

Consumers in the Global South face an impossible choice between subsistence and other living expenditures.

At the same time, food price volatility on international markets puts staples out of reach of consumers in low-income countries. From 2020 to 2021, food price hikes on the international markets contributed to 40 per cent of consumer price increases in lower-income countries. While the pandemic delayed deliveries and caused the cost of international freight to rise, the latest data assessment shows the impact of this disruption on food prices was marginal compared to the recovery of demand from large markets like China. In fact, the price of wheat, maize, and soybeans fell in the first half of 2020 but started trending upward again as demand from China recovered and production levels in the US, Canada and EU dipped.

Hyper-speculation on food commodities disconnected prices from the production and supply context. This financialisation of food markets benefits the minority of grain traders and investors who are reaping record profits in a time of crisis and will continue to do so in the next two years. Farmers in the Global South will never see these profits as they produce basic goods for export and have little power to set prices.

Fertiliser shortages further contributed to the rise in food prices in 2021. This shortage was mainly brought on by restrictions on fertiliser export. Fertiliser export bans by countries like China drove prices up by 50 per cent before the war. Even as the food crisis deepened, 15 national governments imposed a ban on food exports – restrictions that affected the distribution of grain and vegetable oil staples. Today, 20 countries have active bans on food exports.

Loss of purchasing power, economic downturn, and high food prices combined to put 811 million people into food insecurity by 2020. According to the UN, that is 100 million more people than in previous years and one in 10 people globally went to bed without sufficient food in the first year of the pandemic.

Besides these drivers aggravated by the pandemic, the Global Report on Food Crises names conflict/insecurity and extreme weather events as the main conditions for the state of generalised food insecurity.

In 2020, more than 20 countries in almost all regions of the world were experiencing instability or violent conflicts, putting 139 million people into crisis levels of hunger. In recent years, extreme weather events have become common. In vulnerable climate change regions, cyclones and flooding from torrential rains threaten to lay crops to waste, and stubborn droughts starve off livestock and crops. In Somalia, Kenya, Madagascar, and Afghanistan for example, record-breaking droughts have cut grain yields, killed livestock, and sent prices reeling. Below-average rainfall in the 2022 rainy season promise to prolong these conditions. In Pakistan where the disruption to Ukrainian grain imports has been acutely felt, flash floods from monsoon rains this summer have destroyed 2 million acres of crops, disrupted supplies, and sent prices reeling.

Loss of purchasing power, economic downturn, and high food prices combined to put 811 million people into food insecurity by 2020.

These shocks vary in intensity in different countries but the global picture shows that conflict/insecurity is the predominant driver of crisis levels of food insecurity. In some “hunger spots”, these shocks intersect to constrain access to food. In South Sudan for example, extreme weather events, conflict, and economic recession put 2 million people in an emergency food crisis and will push over 7 million into catastrophic levels (starvation and death) of food crisis. Similar forecasts have been made for Somalia whose food crisis is also driven by these factors intersecting.

Taking a short to a longer-term lens on the current food crisis, it is clear that the food security of millions in the Global South is concentrated in the hands of few key international players and at the whims of human-made shocks, including pandemics, climate change, war, geopolitics, and economic recession. Casting our minds to the period before the war also helps us understand that even if the war ended today, the food crisis would continue.

The enemy is the design

Without a view of how food systems are designed and integrated into world markets, we fail to understand that the food crisis is more structural than the war in Ukraine or the aforementioned drivers; it stems from a long-standing process of globalisation, commodification, and financialisation.

Despite the shocks to food systems, food production globally has been on a rise. Europe produced over five times more grain than Africa in 2021. China and India are the highest producers of wheat and have high levels of grain in storage as a long-standing food security strategy. But these stocks do not reach those who need them most for several reasons, including waste, significant amounts being diverted for feeding animal stock or producing fuel, market decisions based on profit, and policy decisions. Most notably, 62 per cent of grains Europe produced from 2018 to 2019 went to feeding its livestock.

In a highly industrialised, specialised, and export-driven food system, countries in the Global South may have high production outputs but in food categories that are non-essential to the diet of their population. Vietnam, Peru, Côte d’Ivoire, and Kenya produce high levels of farm products such as coffee, asparagus, cacao, and flowers. Egypt, which is one of the most impacted by supply cuts from Ukraine, produces high-value fruits on its limited fertile land along the Nile predominantly for sale on the global market.

The food security of millions in the Global South is concentrated in the hands of few key international players and at the whims of human-made shocks.

Many countries were forced into these categories of production and import dependence by Western colonialism. Colonial administrations forcibly seized lands from people, forced populations into a wage labour economy, and introduced the industrial production of cash crops including invasive species. This model guaranteed that it paid to farm cash crops at scale for international markets.

In Kenya, the Nobel Prize laureate and environmental icon Wangari Maathai explains in her memoir Unbowed how the British colonial administration forced many into a deathly wage economy or to convert the farms that fed them into coffee, tea, or timber plantations. She also connects commercial farming and British colonialism’s disregard for indigenous practices to the environmental disasters and malnutrition experienced in modern Kenya.

With the help of unequal trade deals, fiscal reforms and development policies, as well as ruthless expansion of transnational corporations, these legacies have been engrained into food systems, often protecting interests and profitmaking in the Global North at the expense of food security of millions in the Global South. It is in this context that food corporations and grain firms can make record-breaking profits amid a food crisis.

From this perspective, the story of the food crisis is clearly that of flawed design, human-made shocks, and a chronic distribution problem. Undoing the environmental damage and human cost of this globalised food system is the way to go.

Unmaking the food crisis

Announcing an EU funding package for food crisis relief, EU Commissioner for Crisis Management Janez Lenarčič stated that “Millions of people are already affected by the drought and in need of life-saving assistance. In addition, the dependency on Ukrainian and Russian imports already adversely impacts food availability and affordability. The time to act is now. The international community, humanitarian and development partners, national authorities and communities must save as many lives as possible and work together in a sustained effort to address the emergency and build future resilience.”

Despite the meagre funding attending this announcement, there are a few positives within it. First, the EU is showing itself to be committed to strengthening the crisis response and resilience of partner countries. This is important in the face of Russian propaganda assigning everyone but itself blame for the food crisis. Second, it also shows the EU looking at the crisis beyond the lens of the war in Ukraine.

However, the complexity of the food crisis calls for responses that do not begin and end with humanitarian funding. The flaws of a food system that breeds hunger and malnutrition cannot be fixed with reactionary policies; it needs transformational internal and external policies organised around the idea of food sovereignty and that also address the EU’s role in the cycle. This includes weaning food production in the Global South off fertiliser, incentivising regenerative food production practices and production of essentials as close to the consumer as possible, re-routing food surplus to the World Food Programme, investing in climate adaptation in agriculture, and cancelling debt for the countries likely to default on loans amid the economic recession.

These policies are within the EU’s powerful toolbox of trade agreements, development aid, and internal agricultural policy. It is up to it to use them. Statements made by EU Commissioner for International Partnerships Jutta Urpilainen in the wake of the food crisis show its leaders understand this challenge and the instruments at their disposal. But whether action to meet the scale of the crisis will be taken remains to be seen. With Russia deploying its propaganda and “wheat diplomacy” on the Global South to secure its influence, the EU cannot afford to look on indifferent.